Bitcoin rarely goes to sleep like this, and low volatility is certainly not something the asset has a reputation for. Volatility is of course a dynamic beast, and it ebbs and flows throughout the cycle. However there is a simple principle that markets tend to adhere to over time, and Bitcoin is no exception:

Range expansion lead to range contraction - this means that trending rallies or sell-offs are followed by a period of consolidation to digest the move.

Range contraction leads to range expansion - once the market has consolidated long enough, it eventually breaks into a trend in some direction.

The interpretation of this framework related to today, is that low volatility (range contraction) is an indicator that higher volatility (range expansion) is very likely on the horizon.

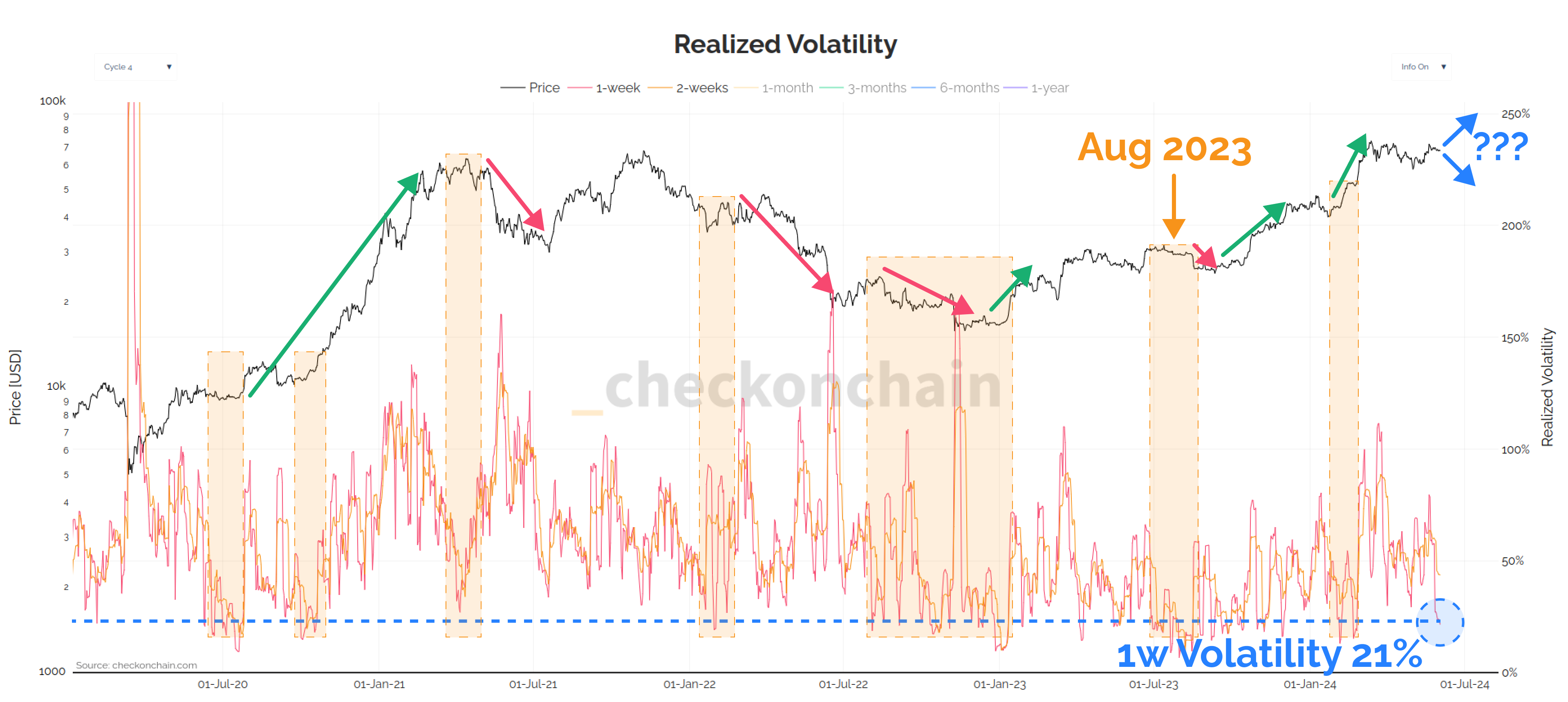

The last time I recall volatility compressing like this was in August 2023, and I prepared/edited two reports for Glassnode covering how derivatives markets and onchain data were pricing this in.

The takeaway of that study was that a big Bitcoin move was well overdue, and downside was poorly priced in. The market the proceeded to sell-off from $29k to $26k in short order. There are many of the same conditions in play today.

Disclaimer: This article is general in nature, and is for informational, and entertainment purposes only, and it shall not be relied upon for any investment or financial decisions.

Keeping One Eye on Macro

With this as context, I want to set the scene with a couple of macro charts that caught my eye this week. I promise not to not add to our boredom, however I sense we’re nearing a key decision point in global markets.

Whether we like it or not, the US Dollar, US treasuries, and oil remain the three most important markets, as they heavily govern the tightness of financial conditions.

The US Dollar is the global reserve currency, and when it gets expensive, countries and corporations have a harder time servicing their debts.

Treasury bonds are the global reserve asset which act as the worlds default savings vehicle, and form the foundation collateral supporting financial markets.

Oil is the energy lubricant which keeps the world turning. More expensive oil prices directly affect the bottom line as a primary input cost for productivity.

For the time being, oil prices are range-bound, and I sense are a lesser part of the current story. The US Dollar is at a decision point. If it were to break lower, it would ease financial conditions overall, likely to the net benefit of assets like Bitcoin. However, should it continue higher within the established 2024 uptrend, it could portend signs of stress, and tighter financial conditions in the near-term.

My instinct is that the dollar is going to be managed lower over the medium to long term, but this weakening may require near-term dollar strength and stress as the catalyst.

The big one however is the US treasury market. Many analysts interpret Powell’s ‘higher for longer’ to mean the Fed Funds rate, but I believe it includes the following:

Inflation is structurally sticky, and will be higher for longer.

US bond yields may be mis-priced and will also be higher for longer.

The US 10y Treasury is the de-facto global reserve asset, and yields have continued to grind higher within an established uptrend all year. When bond yields trade higher, it also means bond prices have traded lower. Since the US-10y sits at the foundation of the global financial system, higher yields mean tighter conditions, less valuable collateral, and a reduced overall risk tolerance.

I’ve flagged in red the severe sell-off we saw in bonds between August and October 2023 on the chart below. During this time, US-10y yields approached 5.0%, equities sold off by -10%, and Bitcoin sold off -12% in one day. That said, BTC then consolidated for two months, and ripped +30% higher.

10y Yields trading up towards 5% is where the Fed and Treasury have previously become concerned about treasury market dysfunction, and stepped in to arrest the fall in prices. This is a reasonable argument for why Bitcoin sold off initially, but then rallied higher afterwards.

The bond market is the one that gets to ‘call time’ on risk assets and financial stability. Should yields accelerate higher from here, it starts getting close to the territory where things could get hairy, and fast.

The setup here is that we should keep one full eye on the possibility for near-term down-side volatility across all markets. The medium to long term result will be the same, they will print the money, and fill any gaps that open up. But on a shorter time horizon, these charts have me just a little bit cautious.

Expecting chop-solidation remains my base case for now, however the probability that we are approaching another range expansion is rising quickly.

Pricing Volatility

Similar to the Glassnode reports I referenced earlier, let’s step through the story being told by both price, derivatives, and onchain datasets.

Realised volatility over a 1-week window has dropped to just 21%, which is about as low as it gets. We can see examples of similar low volatility periods over the last cycle, which usually precede a bigger macro move in either direction.

Note August 2023, which is the most relevant example, where BTC traded -12% lower, consolidated, and then went on a tear higher (partly driven by news of ETF approvals).

The Bollinger Bands are also relatively compressed, with the upper and lower bands separated by just 12.6%. This chart highlights periods with tighter bollinger bands in orange, and two distinct market regimes jump out:

Early Bull markets like 2016 and 2020, which were both Quiet and Trending market structures like we have today.

Late Bear Markets like 2018-19 and the tail of 2022, where seller exhaustion and extreme apathy are on the menu.

Near identical zones stand out when we compare the 30-day price range that the market is trading within.

All things being equal, it is more likely that Bitcoin is still within a Quiet and Trending uptrend on the macro scale. If we were to get any kind of sell-off in the short term, August 2023 may give us a roadmap for what to expect (i.e. it didn’t break the bulls).

From the onchain front, this is where the Sell-side Risk Ratio is my go to metric. This fancy looking oscillator is a personal favourite of mine, and it is constructed and interpreted as follows:

When price is consolidating, traders and investors eventually take all the profit and loss they were going to take in this price range. Once they reach this point of sell-side exhaustion, the remaining holders are signalling that they need the market to move somewhere else to motivate spending.

If the market rallies, they take profits again. If it sells off, some will panic and take the loss.

High Values mean the market is NOT at equilibrium, and significant magnitudes of profit and/or loss are being locked in relative to the market size. Investors believe the price is too high (profits) or fear it’s heading lower (loss).

Low Values mean the market has reached a state of equilibrium, and all the profit and loss that was going to be taken, has been. It is time to move to a new price range to motivate the next wave of spending.

The short-term holder Sell-side Risk Ratio is dropping rapidly (in log scale), suggesting the market has exhausted its sell-side. This is an indicator that equilibrium is close to being reached, and signals we should expect a bigger price move is incoming.