When The Government Pulls The Rug

The Australian government just announced sweeping changes to how they want capital gains to be taxed moving forwards, and it is nothing short of a rug-pull for Aussie Bitcoiners.

G’day Folks,

If you are fortunate enough to know an Australian Bitcoiner, and consider them a friend, I’d kindly ask you to sink a few tinnies in our honour, as we’ve all had a bit of a shit week.

The gubermint who runs the show in The Land Down Under just announced sweeping changes to the tax policy, pitched under the guise of giving young Australians a ‘fair go’, and making it easier for them to buy a home.

Ironically, and totally unsurprisingly, the proposed changes look set to make it considerably harder for young people to save for a house, ensuring much higher tax rates are applied anytime, and everytime you make a return on your capital.

To their credit, I can certainly make the case that these changes will go a long way towards the government’s intended result of making the system fairer for everyone…

…by making each and every Australian poorer through higher taxation, we will indeed become more equal…just in the wrong direction.

Today’s post is partially a cathartic exercise for myself, a eulogy for our collective future tax returns, and hopefully an interesting tale that non-Aussies can learn from.

I want to run the numbers, and demonstrate why this latest government rug-pull will only make the situation for young people saving for a home worse, and not better.

Disclaimer: This article is general in nature, and is for informational, and entertainment purposes only, and it shall not be relied upon for any investment or financial decisions.

TL;DR Summary

Today’s post is a little different, but was something I had to get off my mind, as it was blocking my analytical process. This is a study demonstrating why the new tax policy proposed by the Australian Labor party, hinders, not helps young Australians who want to buy a home.

By abolishing the 50% capital gains tax discount on shares, ETFs and Bitcoin, and replacing with CPI indexation of the cost basis, they effectively kick out the rungs of the asset-ladder which must be climbed just to get onto the first rung of the housing ladder.

The higher the growth of the asset someone buys, the more this new system trends towards a doubling of their effective capital gains tax. It adds several years to the savings sentence for a house deposit, and extracts multiple years of expensive school fees from our children.

The indexation method only benefits investors who buy poor performing assets which don‘t grow at all…like government bonds. In that small sliver of poor performing assets, yes, the new indexation method is better.

For anyone on the lower to middle end on the income spectrum, the new tax policy has outsized impacts on your balance sheet. It doesn’t tax the rich, nor does it help young Australians, it literally targets them, and keeps them lower on the socioeconomic scale.

All is not lost however, and the more political backlash we generate, the more likely some portion of these changes will be in retreat. The Australian Bitcoin Industry Body even has a tool to send emails to your policymakers.

I prepared this piece because it feels like the right thing to do, both personally, professionally, and as a proud Australian. I’m young, I’m an Aussie, and I have an infant son and family in hand.

This budget is a disaster for our finances, and even more so for future generations who receive no benefit from the existing 50% CGT discount.

It’s a scam, it’s a betrayal, and its 100% un-fucking-Australian.

Watch The Video Version

Why You Should Care

We live in an age where sovereign nations are bankrupt, and political polarisation is trending higher, not lower.

We also live in an age where the average attention span is shorter than a TikTok video, and far too many people believe the headlines they read, and can’t, won’t or don’t know how to parse reality from the propaganda.

One reason I am writing this piece, is because it has been bugging me all week, and it was becoming a blocker for my analysis process.

The other reason is because Australia is not the first, nor the last place that taxes will be raised in such an environment. As many Bitcoiners know, governments tend to levy taxes in sly and roundabout ways, with inflation being one of their preferred mechanisms as it is difficult for the average person to reason about.

If I was to give the Australian government one piece of deserved credit, at least they had the balls to levy a straight up tax hike, and break more than a few election promises to do so (even if they dressed it in a ‘woe is thee’ narrative).

They hid it amongst a bunch of fluff about housing affordability, but at least they’re running the political gauntlet.

That’s where my praises for them end.

I’ve spent countless hours thinking about this Fourth Turning decade. I have pondered what higher inflation would feel like, considered deeply how I will try and protect myself financially, and puzzled over what it means for the wider world moving forward.

It’s one thing to think about, and another when you get punched in the face by it.

For non-Australians, I certainly hope this saga offers you a light into what could be in the pipe for many of us in the years ahead. Higher taxes, whether directly, or indirectly via inflation are going to be a very regular character throughout this chapter of world history.

OK, So What’s The Problem?

The Government!

No Check…What’s The Tax Problem?

Right, sorry…

The short story is that Australians currently get a 50% tax discount on any capital gains which are held for at least one year. If I was to buy 1 BTC for $50k AUD in 2024, and sell it today for $110k, I would have made a nominal gain of $60k.

Since I held it for more than one year, the taxable portion of that is halved to $30k, which is added to my overall annual income, and taxed at my marginal tax rate.

This system creates incentives for people to save in assets, hold them for longer periods of time (which lowers our time preference), build wealth slowly and steadily, and also provides capital to support the growth of businesses and the economy.

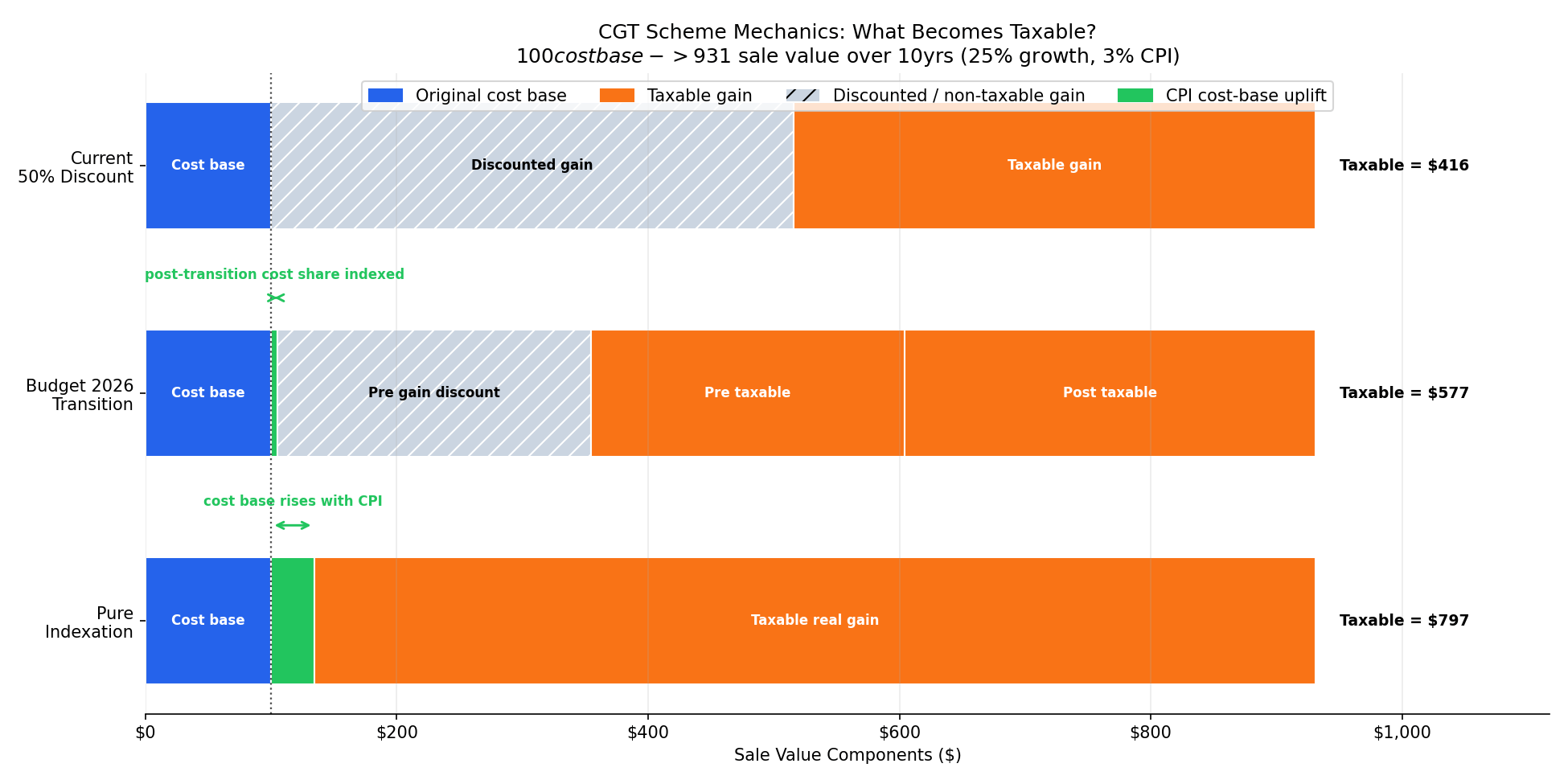

The latest budget handed down by the Labor party on Tuesday night proposes to eliminate this 50% capital gains discount in favour of two components:

Investors can raise their cost basis by the inflation rate each year such that they are only taxed on the real gains.

Imposed a minimum capital gains tax rate of 30% to catch folks who may have small incomes, but live off selling down their asset portfolio.

They are also implementing a partial grandfathering system, where your gains up until 1-July-2027 receive the 50% CGT discount, but all gains after that are via the indexation method.

For my analysis, I will consider these three tax setups; the current 50% CGT discount as the baseline, a transitional system that kicks in July 2027, and the full indexation method which will affect any assets bought from now on.

Now, what is most sinister about all of this, is throughout all of the media coverage of these tax changes, the narrative focus was primarily on housing. The stated intention is to make property more affordable for young Aussies.

None of the media coverage I saw made any effort whatsoever to explain that this was sneakily being applied to ALL assets, including shares, ETFs, and Bitcoin.

I won’t bore you with the details, but suffice to say that this Labor government ran specifically on NOT changing the capital gains and tax treatment for property and assets.

Them breaking that promise barely a year after the election told me that their surveys now show Millenials and Gen Z to be their primary voter base, and outweigh asset rich older generations. They have then decided to use the cover of housing affordability to sneak in a tax hike across the board.

Why Bitcoiners Are Hit Hardest

There are many problems with this cost basis indexation method, but the big ticket ones as I see them are as follows:

Your unrealised gains on 1-July-2027 are locked in at the 50% CGT discount. If Bitcoin has a bad month leading into that date, it can significantly increase our tax rate on the road ahead.

As a call to action, please help us Aussies out by buying as much Bitcoin as humanly possible over the next 12 months to moon the price.

Given Bitcoin is a high growth asset, the 3% inflation rate they measure via CPI is insignificant relative to the price gains. The same logic is true for any high growth asset. As a result, the new tax system disincentivises investing in innovation and growth, and favours investing in poor performing assets that don’t grow at all (like government bonds).

They can raise taxes by underestimating CPI. We all know CPI statistics are nonsense, and massaged lower. The nominal gains of your asset are unlikely to be indexed against the actual cost-of-living inflation rate, but some number cooked up by a bureaucrat trying to obfuscate their other hidden tax of currency debasement.

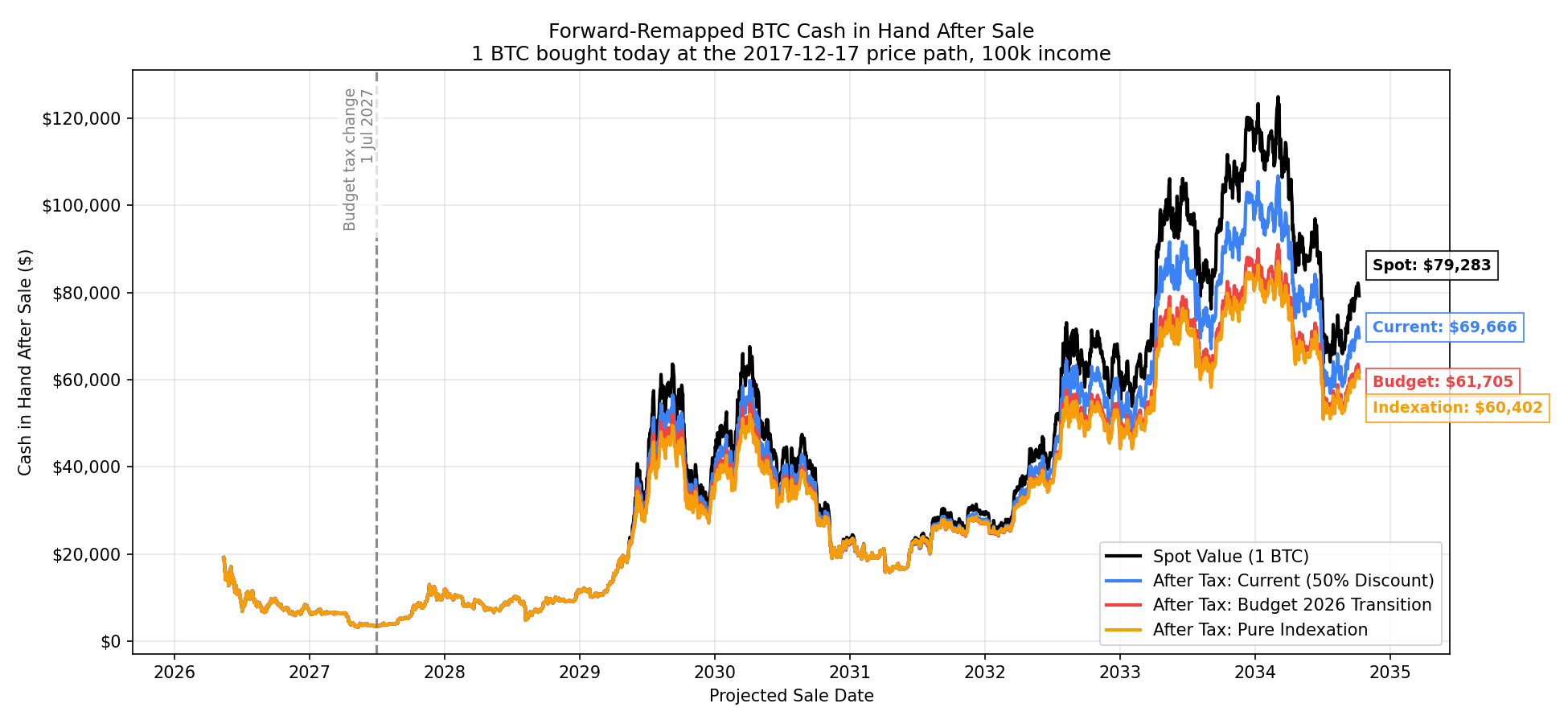

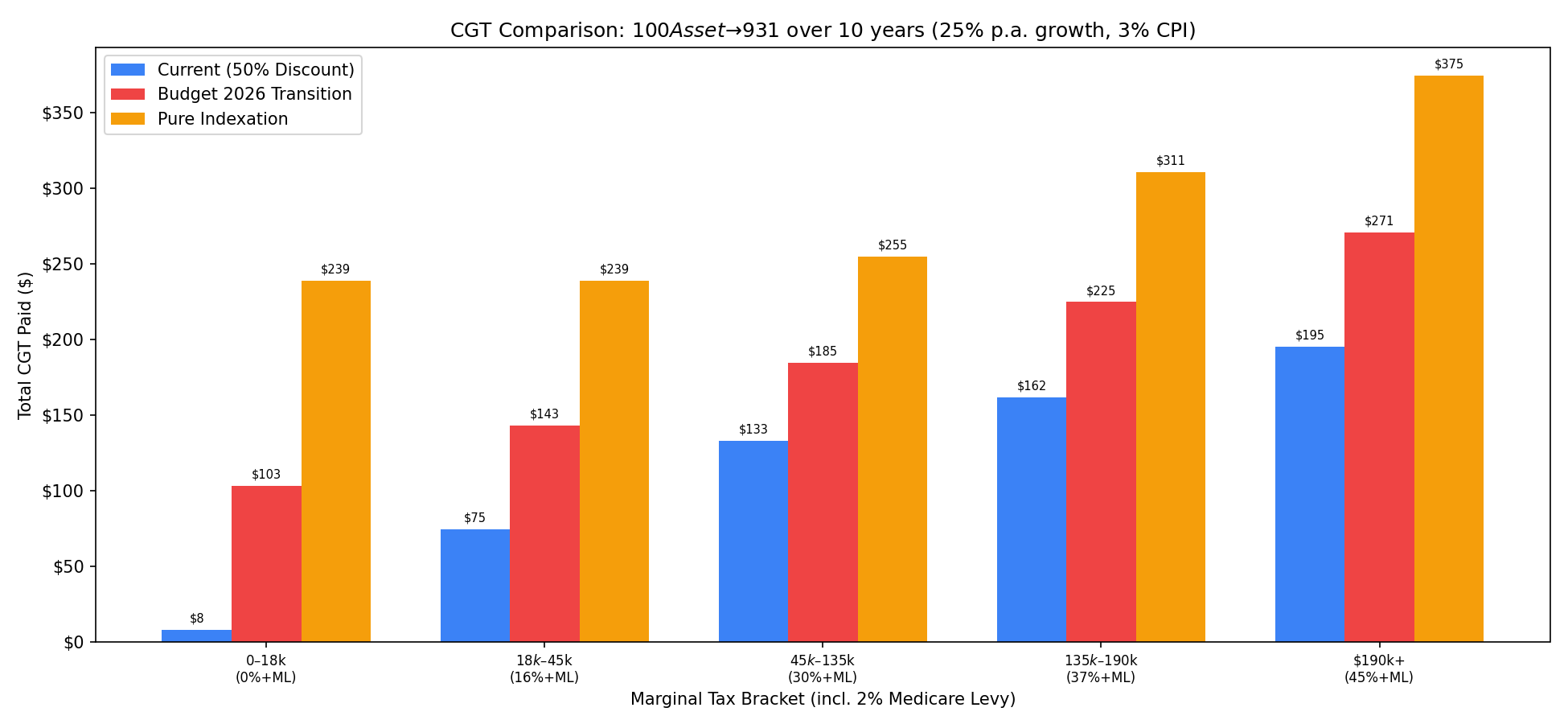

The chart below pretends my first ever Bitcoin buy, which was at the 2017 top, occurred today. I buy 1 BTC at $20k and HODL through all the price history that followed. Assume I have a $100k salary (~20% above national average of $82k). The traces show my net cash in hand, after-tax proceeds from selling the Bitcoin ~8yrs later under the three tax systems:

⚫ Spot Value: $79.3k.

🔵 Current 50% CGT System: $69.6k (12.2% taxed).

🔴 Partial Grandfathering: $61.7k (22.2% taxed).

🟠 Full Indexation System: $60.4k (23.8% taxed).

Bitcoin’s growth outstrips the 3% CPI indexation by so much, that your capital gains tax almost doubles under the new system (12.2% —> 23.8% tax).

Note: I will keep using these three tax systems consistently throughout this report, and consider the current 50% CGT (blue) as the baseline. Full indexation (yellow) is the new comparison given that is the system which will affect young Australians from here onwards.

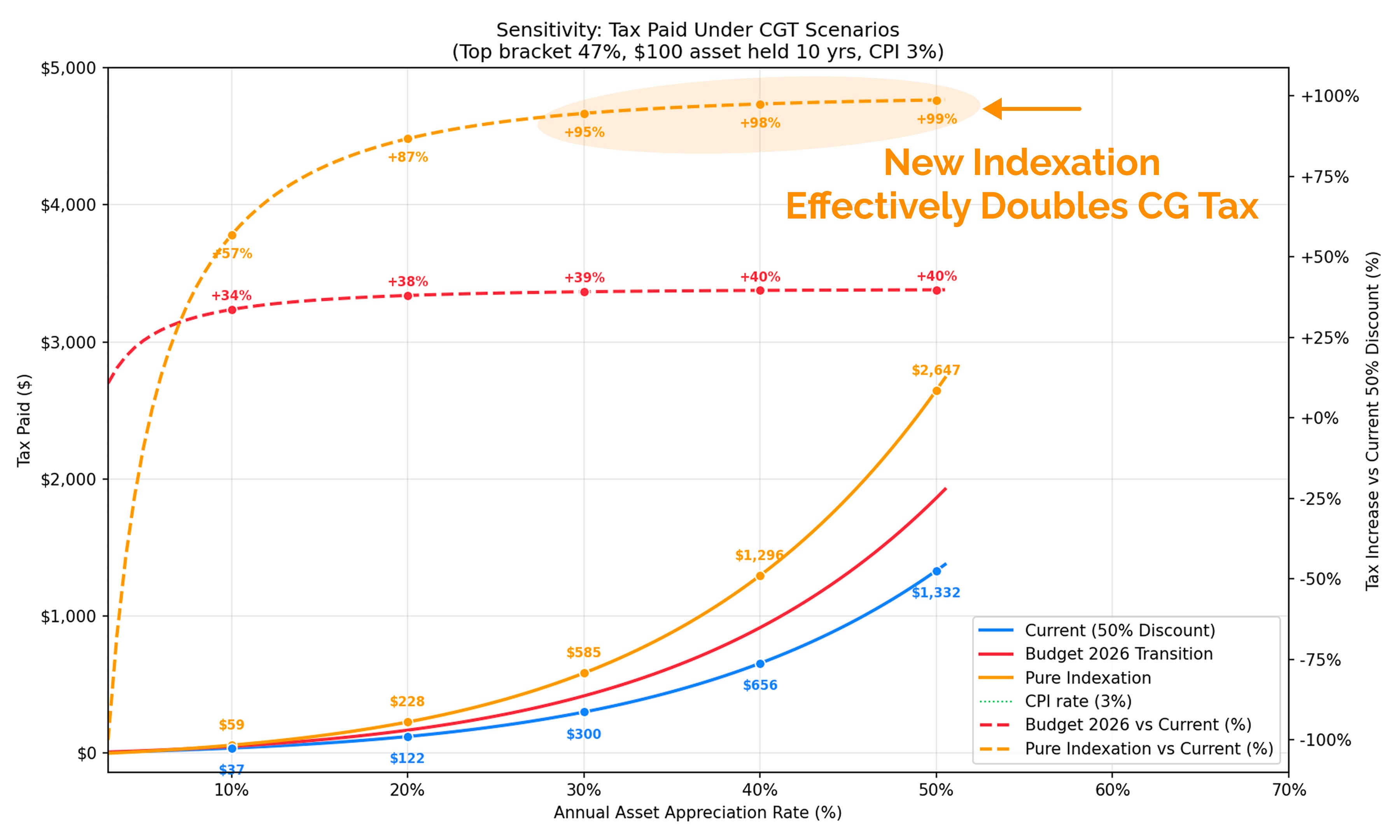

The chart below is a sensitivity study demonstrating how the higher the growth of your asset, the less the CPI indexation method helps you.

Once an asset grows above 20% per year, the new tax system costs you between 87% to 100% more in net capital gains taxes upon sale.

I even watched a 3min clip from the ABC government propaganda arm. In it, they made the extraordinary claim that this might make safe, stable, low growth assets like infinitely printable government bonds more attractive!

I can’t think of anything which would make young Australians better off, than jamming their portfolios full of infinitely printable government debt paper…

Kicking Out The Rungs

When you really cut to the core of the problem, the average Australian property price is now over $1M AUD (~$700k USD), and in order to avoid hefty mortgage insurance, you will need a 20% deposit.

Few folks have a spare two hundred grand lying around, and that means you need to save capital in assets first in order to get a foot onto the housing ladder.

If you save in cash, and stick it in a high interest bank account, you might be lucky to get 4% to 5%. You also take the full brunt of both income tax and inflation. It will take the average young Aussie on a decent salary more than forty years to save just the deposit given historical house price growth rates.

Forty fucking years, to save for the deposit in cash.

The ONLY hope young people have is by saving in assets like shares, ETFs and Bitcoin, and that means you NEED to take risk, and are hopefully rewarded with an outsized return.

You need to climb the smaller ladder of an asset portfolio just to reach the first rung of the housing ladder.

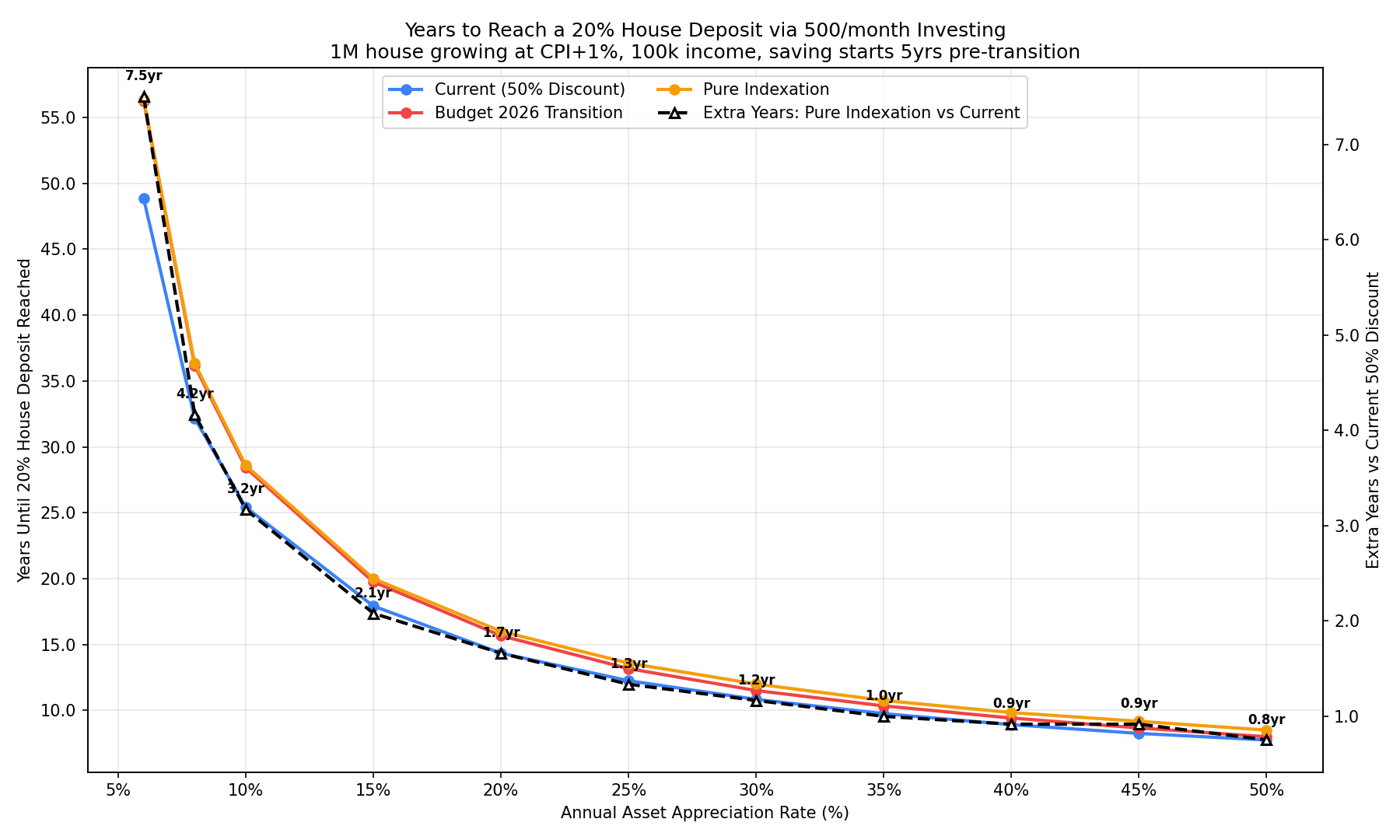

My model below is for someone with a better than average Australian salary (mean is A$82k), who is investing $500/month, and chasing a housing market growing at CPI+1% (which is conservative).

If you’re lucky enough to buy a high growth asset which rips at a totally unsustainable 50% per year non stop…

It still takes you almost a full decade of saving to get the deposit…

…and the indexation method adds at least a year to your sentence because of how much the extra tax eats into your proceeds.

For the diligent saver, the new indexation system adds between one and five years to the saving timeline for a young Australian to reach their deposit.

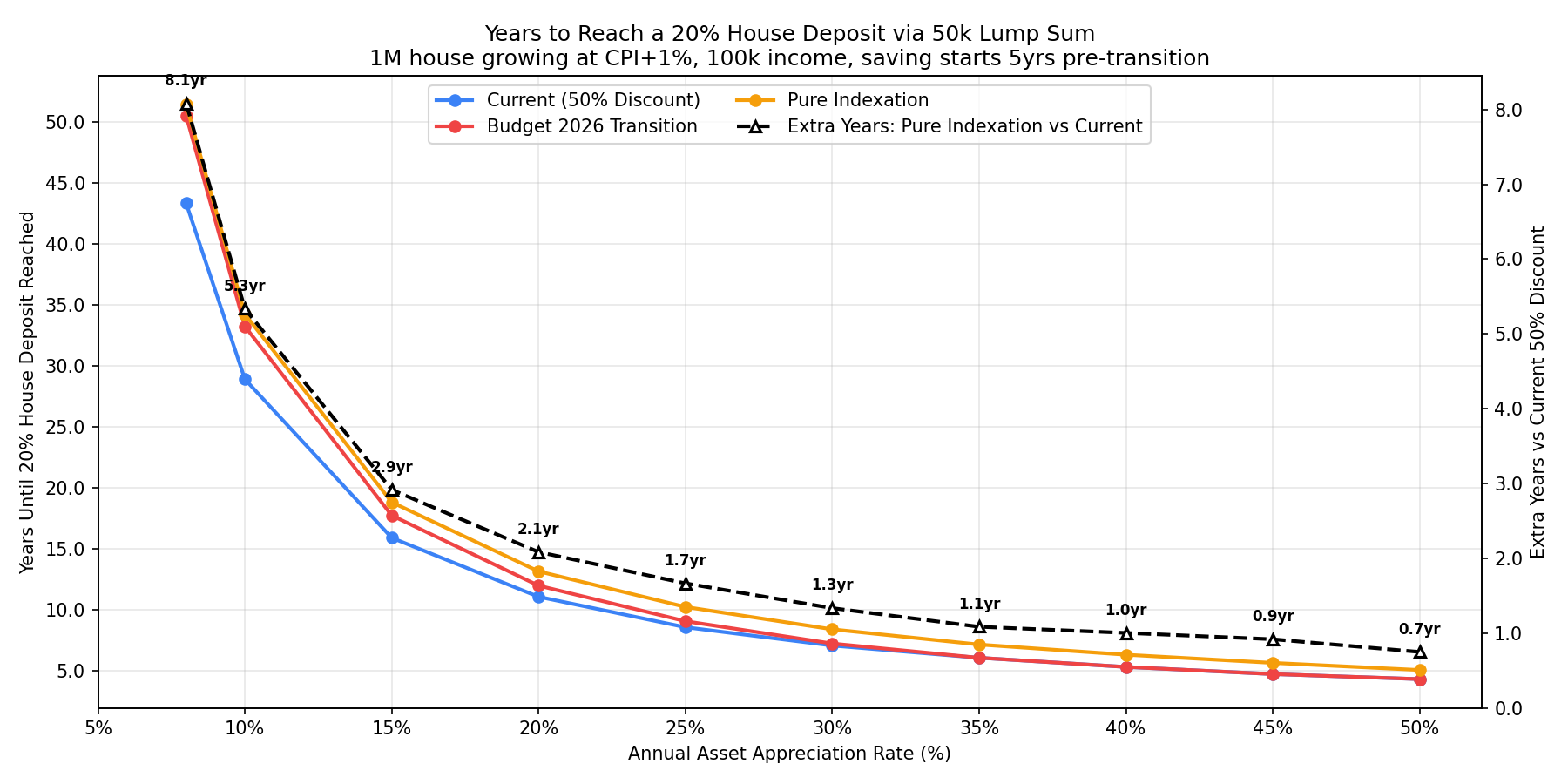

If you lump sum $50k and allow that to appreciate in pursuit of a deposit, the problem is even worse, because capital growth does all of the lifting, not the regular $500 investment.

The new indexation method adds north of five of waiting time for an asset which is growing at 10%/yr, adds at least two years for 20%/yr, and still adds the best part of a year for high growth 50%/yr assets.

The government policy is pitched at improving housing affordability for young Australians.

What it actually does is taxes and kicks the rungs out of the preliminary asset ladder you MUST climb just to reach the first rung of the housing ladder.

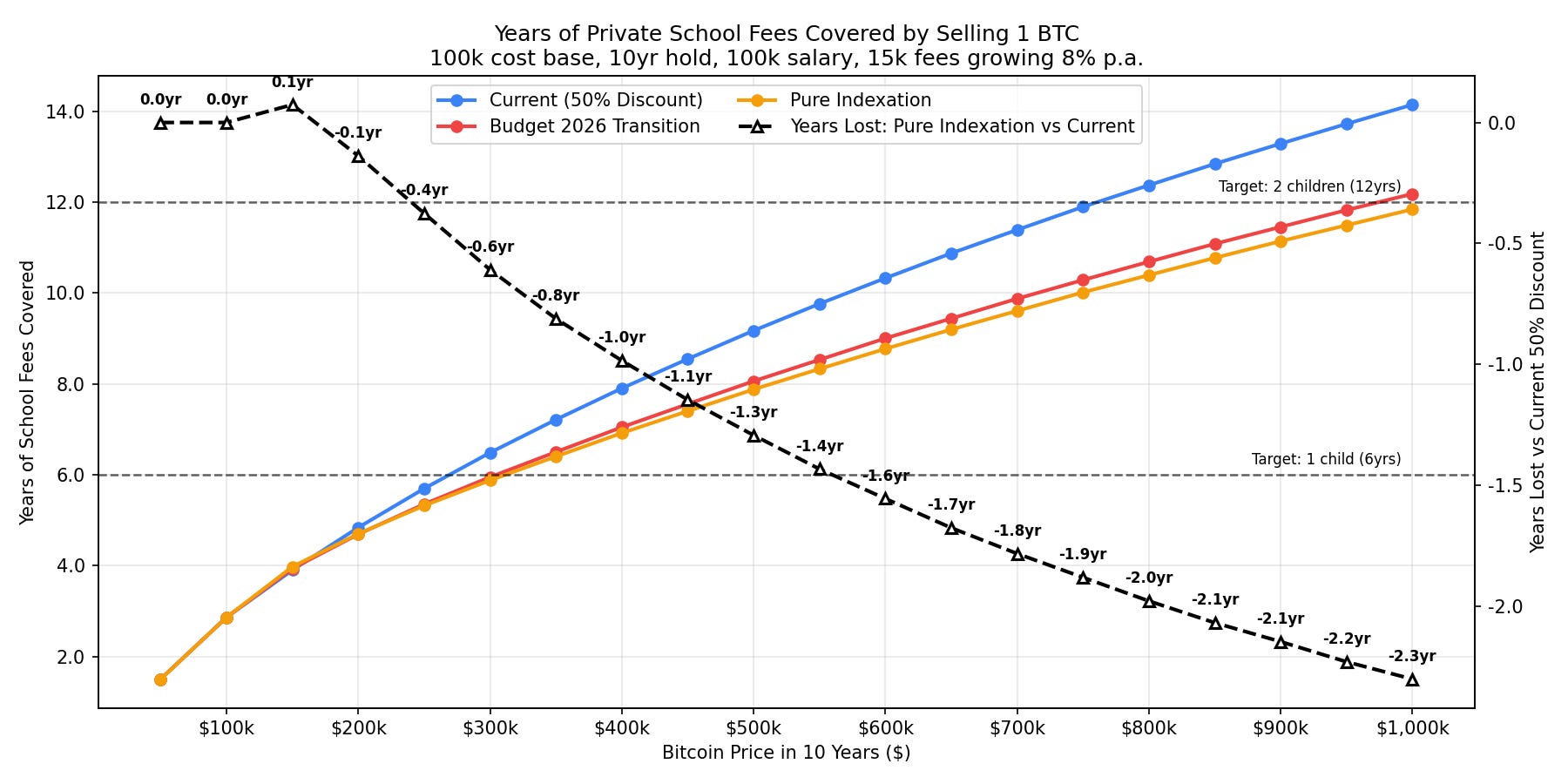

Another tangible case, and one which really hits home for me, is saving money to send your kid to a good school.

Personally, I have allocated some of my BTC specifically for putting my little boy through the 6yrs of high school (secondary education). Fees routinely run at around $15k to $25k per year, and grow at 5% to 8% per year (in line with the actual debasement rate of the AUD).

I asked the question: if I bought 1 BTC today for $100k AUD specifically allocated for school fees, what price does it have to reach, such that I can sell a chunk each year and cover all six years?

The second question is, how much does the government’s new tax policy help hinder me in achieving this goal?

Bitcoin has to reach around $270k for me to do this for one child, which is well within reach and reason.

The governments new tax policy reduces my run-way by about 10-months of school fees, so the Bitcoin price will now have to reach $300k to cover it instead.

If I wanted to send two kids to a good school, I now need Bitcoin to 8x and reach $800k under the current 50% CGT discount scheme.

The new government tax policy strips away 2 full years of school fees (one per child) in tax relative to the current system, which I either have to fill the gap with more taxable income, or wait for BTC to reach $1 Million instead.

Thank. You. Very. Much.

Winner Winner, Chicken Dinner!

Young Australians are early in their careers, have low salaries, little savings, and are trying to enter a highly inflated housing AND asset market.

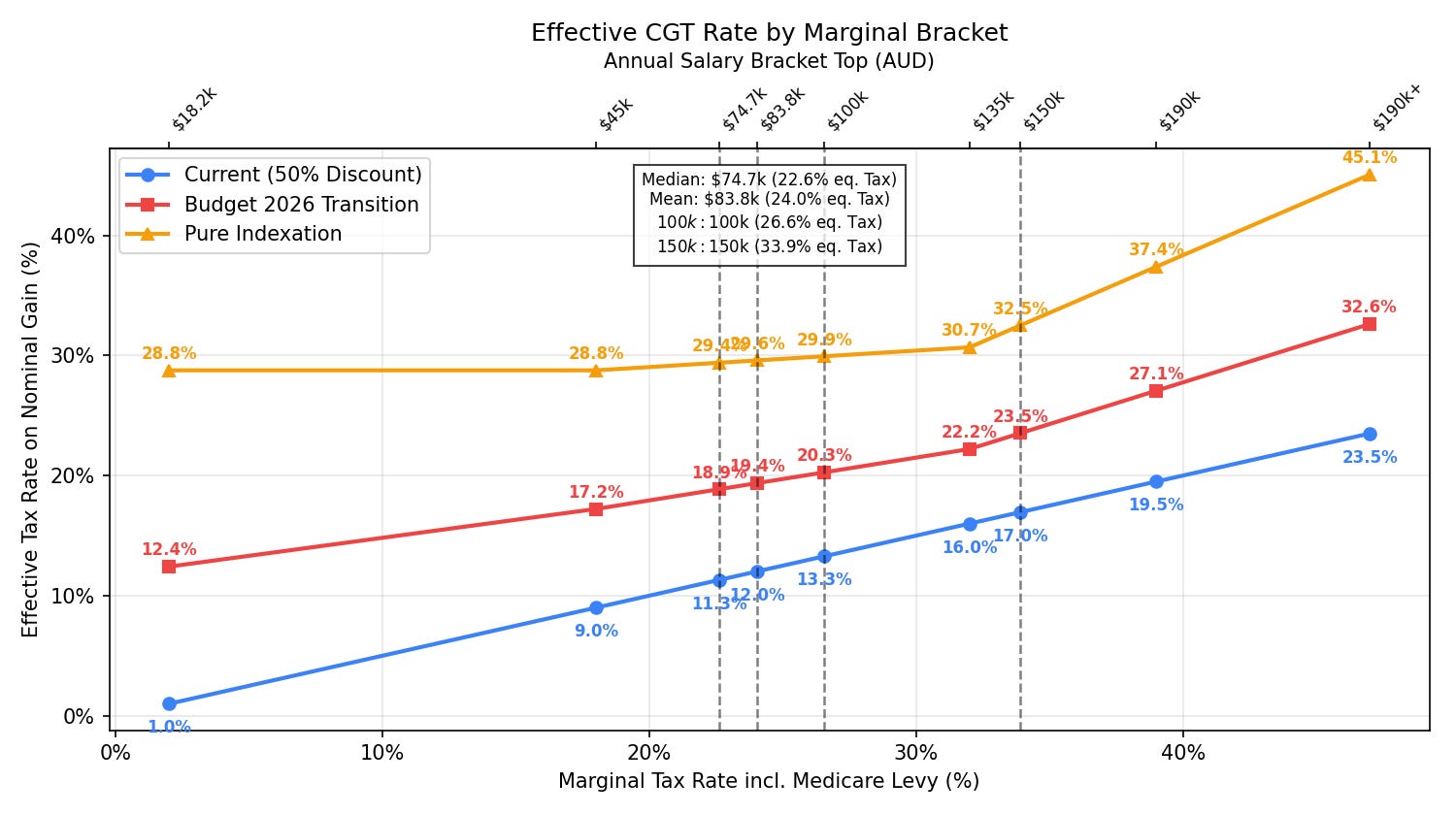

The new tax policy ensures that the ladder to get on the ladder is taxed at ~30% even if you’re earning what is a below median (A$74.7k) or mean (A$83.8k) salary.

You would otherwise see an effective capital gains tax rate below 12% under the current system.

For the folks who support this policy, because they want to ‘tax the rich’, just note that absolute tax applied under the new system (orange) on every dollar invested is considerably higher for lower income brackets, than for higher ones.

I can only assume the government has tried to target wealthy retirees, who are selling down portfolios rather than earning a salary income. What they are actually doing is ensuring the people who have the least savings are taxed at a considerably higher rate, and are thus forced to remain lower on the socioeconomic ladder.

The current 50% CGT discount compounds with the low marginal tax rate to help low income workers the most, delivering the lowest overall tax rate.

The new system successfully makes everyone poorer, and ensures the folks who are barely making ends meet…stay there.

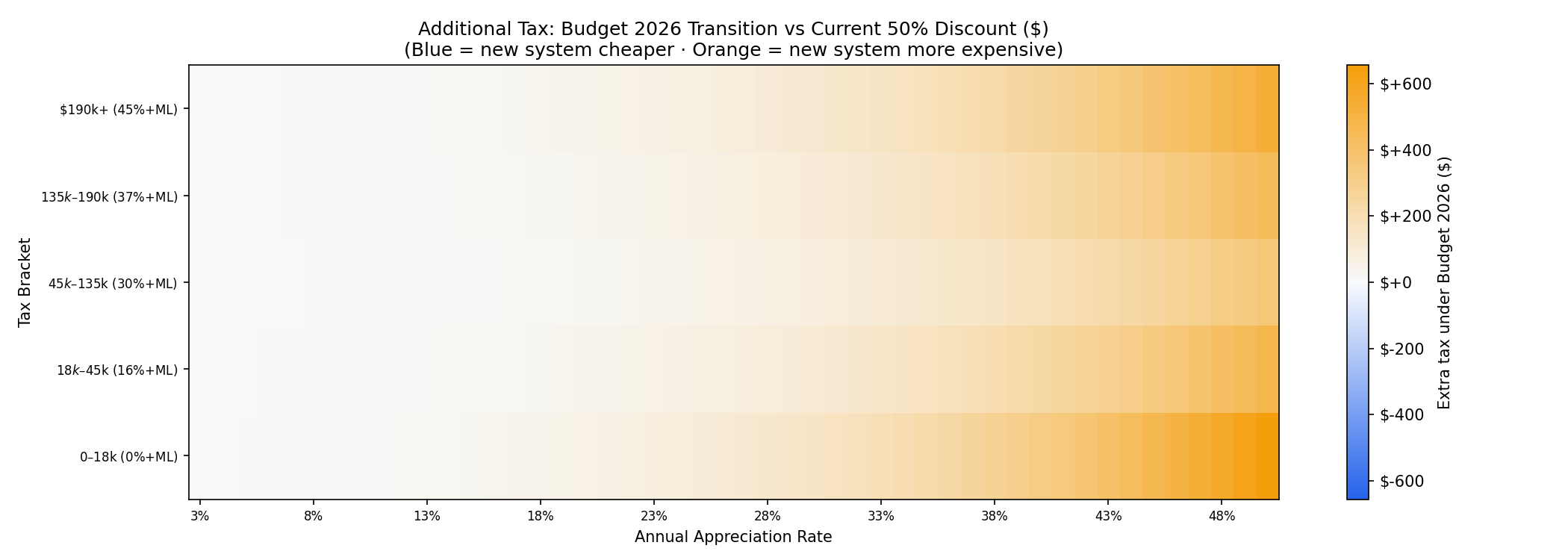

I ran a sensitivity analysis based on the Australian tax brackets, relative to the appreciation rate of the asset purchased. The aim is to see which people and conditions benefit from the new capital gains tax under the indexation system.

The orange part of the heatmap is where the new system is strictly WORSE for an Australian investor.

The blue zones…if they existed…would show instances where we are better off.

To be very fair, if you buy government bonds which get rekt by inflation, you are actually better off under the new system. The scale of that benefit is just so low, it is indistinguishable from the zero line. That is primarily because you made no money on the asset, but perhaps that is the point of the policy.

Nobody actually wins under this new tax system except the government, lawyers, and accountants.

It Cannot Be Incompetence

There are usually two conclusions when it comes to bad government policies:

Incompetence.

Malice.

Whilst I know there is plenty of room for door number two, I generally give the benefit of the doubt, and ascribe a lot of it to door number one.

In this instance however, I cannot give them that pass.

It took me approximately 5-seconds of thought to intuitively realise something wasn’t right when I started hearing about this budget.

It took me 10-minutes of prompt engineering to get the bones of this analysis in place, and to satisfy myself that the numbers confirmed my suspicions.

It is impossible that the Labor government broke these widely publicised election promises, so blatantly, without being fully aware of what I have just written above.

They know housing affordability is great cover for disguised tax hikes.

They know young Australians are pissed at how expensive housing is.

They know the only hope they have is saving in assets.

They know taxing assets more heavily ensures less upwards mobility.

They’ve proposed these tax changes knowing full well it hits the poorer, harder.

They know this system makes everyone worse off, not better.

In this instance, I cannot give them a pass for being incompetent.

If they cannot get a staffer to spend 10-mins with a spreadsheet and an LLM to think through even this rudimentary analysis, then they have no place being in office.

If they can, and did, and know these results, then I’d argue we should be asking hard questions about who they work for, because they are certainly not working in our best interests.

Concluding Thoughts

I genuinely had to get this piece written and out of my mind. It’s currently 1am, and I am no night owl.

Whilst this event is nowhere near the size and scale of this comparison, I can only imagine what it feels like when an emerging market slashes their currency overnight. This tax change effectively robbed 20% to 30% of the value of every Australian investor’s future wealth, and changes the calculus on long-term goals significantly.

I am a young Australian, who is literally saving for a house, and school fees for my son. This budget has added years to my savings plans, and steals 20-30% of my savings wealth I have accumulated over a decade.

Thanks mate, what a true gift that is.

If you’re an Aussie reader, I have no doubt you probably feel just like I do, and it has been a pretty shit week to process.

It has been eye opening, and one of those events you can think about, and theorise about, but it just hits different when it actually comes to pass. It stings like betrayal, not because I trusted the politicians in the first place, but because a move like this one is just un-fucking-Australian.

So what on earth do we do?

First things first, don’t panic, and certainly don’t do anything rash. There is still a long, and winding political road ahead before these changes become legislation.

There will be backlash, and there will be re-negotiation, because it won’t take long for even the most devout ALP shills realise their kids’ futures are impacted.

I am no tax accountant, but I do believe finding a good one will turn out to be an invaluable investment. A wise man once told me that whenever the politicians change the right side of the tax code, a whole world of unforeseen consequences (read: opportunities) opens up on the left side. Life always finds a way.

I’m not one who usually cares about political action in any way shape or form. However there’s an army of Bitcoiners hard at work constructing tools to send emails to every politician with an inbox. In this instance, it might be worth spending 10-mins crafting an email to let them know you’re an unhappy camper.

One email is noise, but a thousand is a voter-base. Each email is indicative of 100 people who didn’t speak up, so the numbers can compound quickly.

Keep it concise, keep it human, tell a story that hits home, and try not to call them a dickhead too many times in the subject line (as true as it may be).

For readers who are not Australian, don’t assume they aren’t cooking up something similar in your neck of the woods. These scheming political thieves know how to hide a tax hike, and they always wrap it in something that pulls the heart-strings of the masses.

This article is my small way of pushing back, and I’ll tell you what, I feel just a little bit better now that I’ve got it out on paper.

Subject Line: Oi Dickhead…Read This Cobba!

Thanks for reading,

James

I'm sorry you're mentally struggling with this; and after reading the article I can completely understand why.

This is an important piece, and it ties in to your brief mention of the Fourth Turning. I'm centered around that narrative and have been discussing it in podcasts. Why? Because I think what you are seeing here is the future, and what is coming will be much more egregious than this.

Systems are breaking as the global debt crises enters the final stage of the Fourth Turning. And as societies lose cohesiveness, fairness, and the rule of law you will see governments enact more legislation like this.

There is no limit to where this can go. In my own nation as the system has collapsed in previous cycles, we have seen suspension of fair trial, imprisonment without charge, outright seizure of assets. And also complete collapse of currencies. During the American revolution the "Continental"... worthless. The Southern states paper in the Civil War... worthless.

Financial repression will soon be the next stage here in the US. If you are not aware of what that is you can read the playbook in the IMF's guidelines.

The last thing I will say is this. As this system strains, all the government has to do is paint Bitcoiners as having unearned wealth. "They were lucky. They got in early. They knew something all of us didn't. They are hiding their wealth. They don't want to share."

Your neighbors won't be in the street to picket supporting you in your attempt to push back.

Now, I don't mean that there is not hope here. In fact, this seems so draconian and affects ALL Australians that I believe people WILL picket over this and write some pretty pissed off missives.

All I'm saying if for Bitcoiners there is a deeper message here to think about.

Best to you, James. Fingers crossed that sharp people like yourself can get this fixed.

Thanks James, you are by far my favourite Bitcoin analyst.

We need to do everything in our power to stop this in it's tracks. It truly is 'you'll own nothing and be happy' nail in our kids future. A government that is pushing socialism as 'normal' in the psyche of Australians, and pushing it in all schools including 30k a year schools. This is a longer conversation, but important.

Back to the CGT proposal on the table. We need to watch this space carefully as Politicians have a way of exempting themselves from decisions that effect us in unfair ways. A couple of examples.

Super Tax changes: Division 296 — ordinary Australians got hit, politicians/judges largely escaped via defined benefit schemes, on a Federal and State level

CGT reform — ordinary Australians get hit on shares, investment properties, etc. Politicians also hold those same types of assets personally, so they would in theory be equally subject to it ...

However, the same constitutional protection issue could resurface at the margins. State politicians and judges on defined benefit schemes won't be affected simply because their retirement wealth is in a pension, not in capital assets — so they're again structurally insulated in a way most Australians are not.

Therefore the message we need to get people to understand is ok for thee but not for me is the mantra of those making these decisions that ultimately affect our quality of life.