Bitcoin Bull Market Blues

Bitcoin has broken decisively below the Short-Term Holder cost basis at $59.6k. This brings the risk of a top heavy market ever closer to a reality, and prompts a deeper look at the situation.

‘You need to know the market's going to go down sometimes. If you're not ready for that, you shouldn't own stocks. And it's good when it happens.’ — Peter Lynch

Disclaimer: This article is general in nature, and is for informational, and entertainment purposes only, and it shall not be relied upon for any investment or financial decisions.

One of the great things about writing checkonchain as an Australian is we get to watch the Bitcoin market nuke while the rest of the world sleeps, and have analysis ready for the rest of the world’s morning coffee.

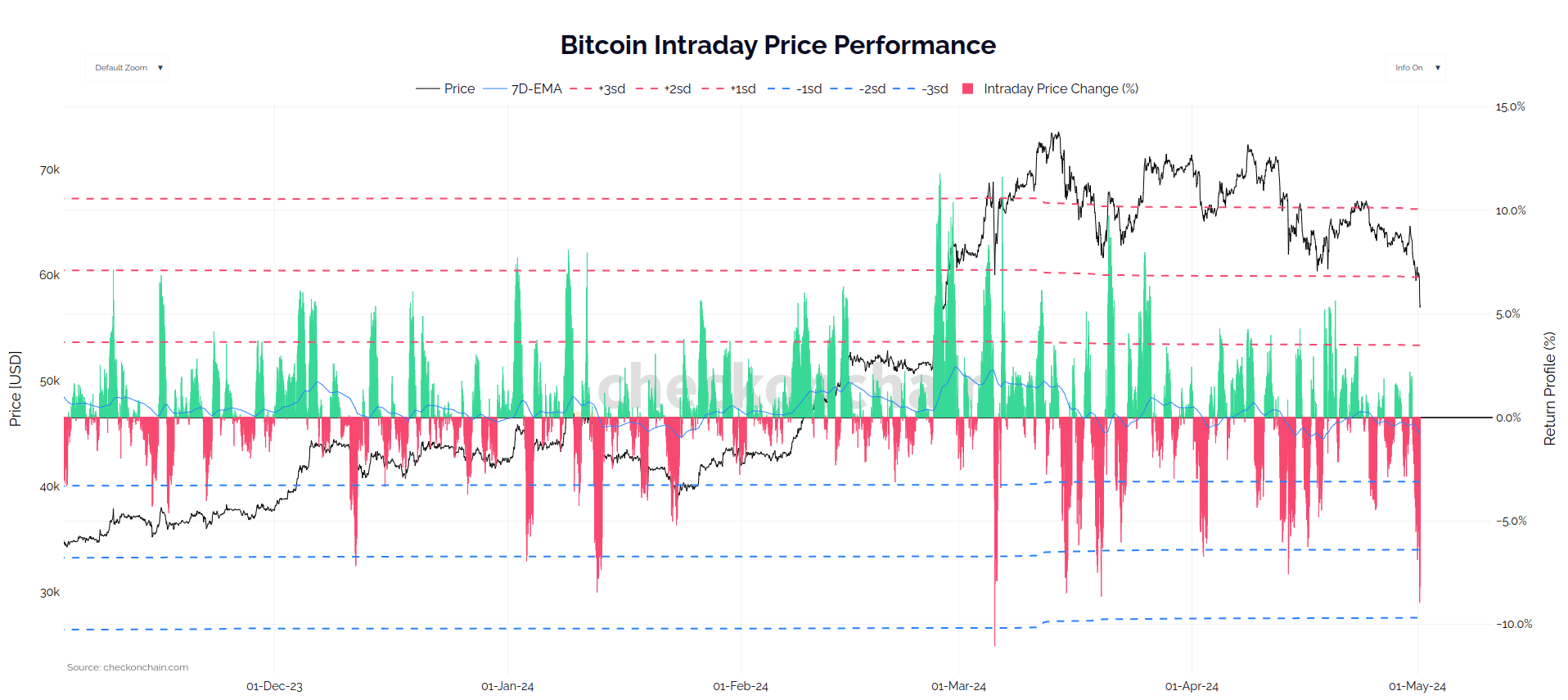

And what a nuke we have on our hands to open the month of May, with Bitcoin trading down -$5.65k (-8.9%) overnight.

Likely of the most consequence is the decisive break below the Short-Term Holder cost basis at $59.6k. As we flagged in our debut report exploring whether the Bitcoin market was Top Heavy, this was an important level as it is synonymous with higher risk environments.

The Short-Term Holder cost basis is important for a few reasons:

It is the average cost basis for recent buyers.

These recent buyers are statistically the most likely to panic.

It delineates a point where a few too many coins and holders are underwater, which can be a deal breaker for bullish sentiment.

Most importantly, breaking the STH cost basis isn’t the end of the world, nor the end of the bull market. It doesn’t help…but it is and has been recoverable.

📽️ Watch Part 1 of the Video Analysis (Free)

Did Derivatives Deleverage…Again?

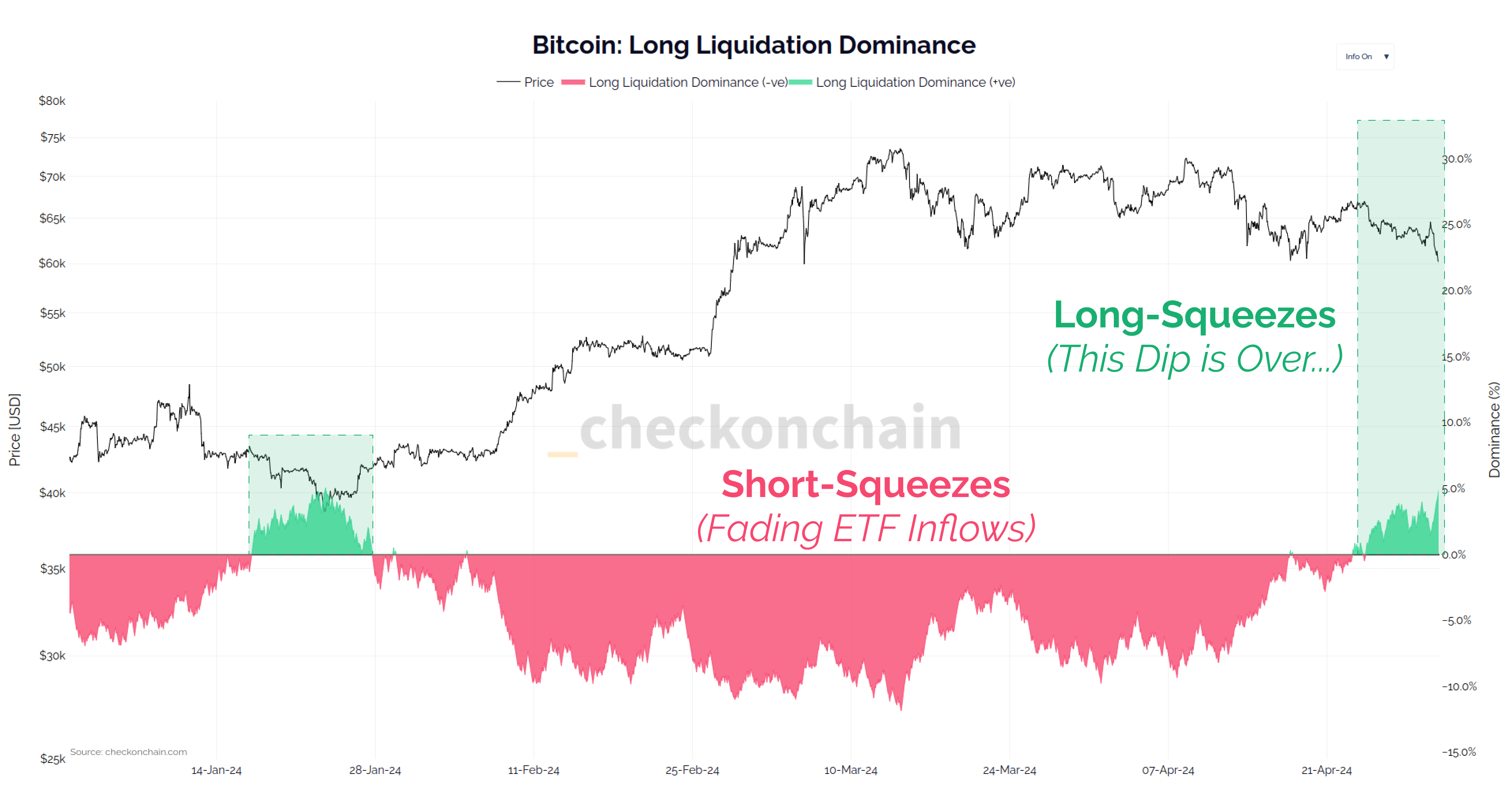

If you were around during the 2021 bull market, you will know that the bull market died in spectacular fashion in May 2021. At the time, 80% of all futures contracts were levered up against BTC collateral. Everyone was levered long, and when the market slipped lower, not only did their futures position fall, but so did the margin they collateralised it with.

The result was a cascading deleveraging event driving BTC prices from $58k to $29k in short order. So when I see a big sell-off like today, I always check to see if derivatives played a role.

At first glance, we can see that liquidation dominance is back into Long-side territory. This tells us that of the people liquidated today, most of the volume was on the long side.

Isn’t it funny that the market thought it was a good idea to fade the ETF rally, getting short-squeezed from $38k all the way up until last week as a result…

…and only after all that success did they decide that now was the perfect time to go long…

However, on deeper inspection, the overall futures open interest doesn’t appear to be excessive relative to the market size. Furthermore, only 40% of the market is coin-margin, which is a huge difference in downside reflexivity relative to the 2021 market.

This isn’t striking me as a derivatives led sell-off.

The oscillator below indicates when a significant amount of leverage is either added into 🔴, or deleveraged out of 🔵 the market over a 7-day period. We saw a degree of overheating as the market rallied into the $73k ATH, but it has cooled down a lot since.

In fact, we saw two micro deleveraging events during the month of April, adding further evidence that derivatives are more likely a minor factor driving the market right now.

Funding rates have also cooled off significantly from the excesses of the ETF launch, and we didn’t see a large negative spike which would signify forced selling.

This sell-off is increasingly looking like it wasn’t a derivatives wash-out, and therefore we should investigate the spot and onchain data for more clarity.

Anaemic Spot Demand

As the Bitcoin market evolves, we must take into account more market dynamics to get a full picture. If we start with the spot markets, we can see that the CVD metric has moved into net-sell-side pressure of around $50M/day.

In other words, there was $50M/day more Market Sell volume today than there was Market Buy volume. This describes the urgency of the marginal investor, and is a stark change from the $100M+/day excess Market Buy volume seen as we ramped into the $73k ATH.

Spot markets appear to be seeing a near-term reversion into sell-side dominance by the marginal investor.

The ETFs have also seen relatively anaemic demand in recent weeks, with around $200M to $330M in outflows per week in aggregate. Of course GBTC continues to dominate these outflows, but they do still house over 300k BTC, and outflows have also come out of several other ETFs over the last two weeks.

The new ETFs are seeing a softer demand profile, with some instruments transitioning towards light outflows. This is within a backdrop of GBTCs seemingly endless sell-side pressure, and is a net headwind for the market.

Top Heavy Risks

Arguably the most important observation is the market falling below the STH cost basis ($59.6k). As it stands, 3.31M BTC are held in loss by the Short-Term Holder cohort, which is a hefty sum and represents 2-out-of-3 of their held coins being underwater.

Note: Our paid subscribers will find our full analysis below, and Parts 1&2 of the video at the end of this report (Part 1 can be found on our Youtube channel).